The U.S. General Services Administration (GSA) has been suffering through budget cuts that have dramatically reduced funding for the construction, acquisition, renovations and even the basic maintenance of federal buildings. This has served to increase the federal government’s reliance on leased space, benefitting private-sector landlords. This article seeks to cast some light on what is really happening with GSA’s budget. As I’ve written several times on this blog, you need watch only GSA’s budget as the bellwether of demand for leased space.

A little background: GSA leases and owns nearly 360 million square feet of space. In the case of leased space, GSA leases from private-sector landlords and, in turn, “subleases” that space through occupancy agreements to federal agencies. In the case of GSA’s owned inventory, it charges market-based rent to the agencies who are its tenants. GSA also charges agencies a typical fee of 7% on top of rent to cover its operational costs. All of these rent and fee revenues flow into the Federal Buildings Fund (FBF), the idea being that the FBF will provide the capital necessary to fund rent to private sector lessors and also to maintain and improve GSA’s own inventory.

The FBF is brilliant in its simplicity…when it works properly. The agencies’ contributions are equal to their pro rata use of space, and the payments provide funds adequate to operate and maintain the federal real estate inventory. But here’s the rub: Ultimately GSA does not control the funds in the FBF–Congress does. Though it is an independent agency, GSA’s budget is still subject to congressional limitations on the use of FBF revenue. Congress has been reducing the available funds–first a little, now a lot.

Frankly, this should come as no surprise. The U.S. budget situation is dire, and cuts have been implemented across the board. Our political leaders have struggled to resolve their budget positions, resulting in Continuing Resolutions and, more recently, Sequestration. All agencies have had to tighten their belts but it seems that GSA’s budget has been hit particularly hard, partly because it’s all too easy to defer repair and maintenance expenses and also because GSA has drawn the ire of its congressional handlers on fronts too numerous to detail here (though we direct the readers to this article, this one, this one and this one to get some flavor for the range of grievances).

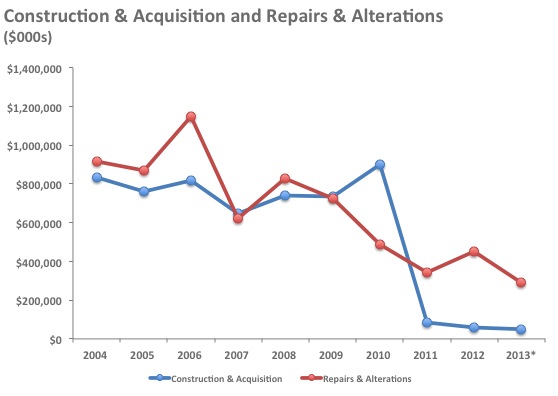

The graph does not include $5.55 billion in ARRA (“Stimulus”) funding that GSA received in 2009.

This graph highlights the fundamental problems. You would expect Repairs & Alterations expenditures to be steady or rising (especially considering that GSA owns more than 1,500 buildings with an average age of 47 years), yet Congress has increasingly squeezed those items as it attempts to restrain the federal debt. The situation with Construction & Acquisitions is even more pronounced. That figure dropped off the end of the table after the Tea-Party stormed the Congress in 2010. With few new buildings entering the federally-owned space inventory, the average age of the present stock keeps growing.

Faced with this “new normal,” GSA has found itself unable to invest in its owned facilities, setting the FBF on a path to insolvency. The federally owned inventory is slowly deteriorating, and because GSA is required to charge market-based rents for its space, those rents are declining. The declining rents further reduce the revenue available for reinvestment in the inventory, and the circle of misery is complete. A 2012 GAO report noted that, due to falling rents and rising operational costs, 30% of GSA’s owned assets lost money in the previous year.

The irony is that Congress’s spending restrictions have pushed the FBF’s ledger well into the black; yet mounting deferred maintenance is sufficient to immediately overwhelm the Fund’s surplus. In fact the 2012 GAO study found that $4.6 billion of repairs and alterations “liability” has accrued in GSA’s inventory (this despite GSA’s earlier spending of $5.55 billion of Stimulus funds, much of it on “greening” its inventory). Further, GSA’s benchmark for annual repairs and maintenance is about 2-4% of replacement value, which calculates to between $900 million and $1.6 billion. The FBF simply does not produce enough income to keep up with these costs, as evidenced by the fact that, in many years, Congress has had to fund GSA above and beyond FBF-generated revenues.

This story doesn’t end well for GSA or its facilities. Yet, lessors will benefit because GSA’s inability to maintain its inventory sufficiently to meet its customers’ needs is driving tenancy to the private-sector where well-maintained, well-managed and well-capitalized buildings abound. This trend will not change unless Congress dramatically improves GSA’s appropriations, and that appears highly unlikely. In lieu of these funds, GSA is doomed to try to bootstrap itself out of this predicament, an effort that has largely failed through the entire history of the FBF.

To view Part 2 of our look at GSA’s budget, click here.