The following post was written by Andrea Cross, Colliers’ National Office Research Manager | USA.

Sources: Bureau of Labor Statistics, Colliers International

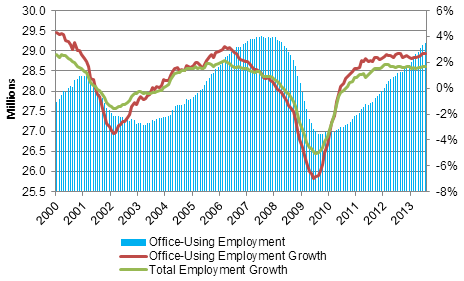

Despite a slow recovery in the office market, growth in office-using employment has outpaced overall employment growth during the last few years. As of July 2013, the primary office-using sectors recovered 93% of jobs lost during the recession, compared to an overall recovery rate of 77% in total employment. When temporary employment (one of the fastest-growing employment sub-sectors during the last few years) is excluded, office-using job recovery is roughly 83%–still ahead of the pace of recovery in total employment. The professional and business services sector has been driving office-using employment growth, exceeding its pre-recession peak by 535,000 jobs as of mid-year 2013. However, the financial activities sector has been adding jobs at a modest rate on a year-over-year basis for more than two years, recovering nearly one-third of jobs lost during the recession as of July 2013.

The relatively slow recovery in the national office market, even as office-using employment approaches pre-recession levels, underscores the impact of more efficient office space usage by tenants, driven by the following factors:

- Economical: a desire or need for cost savings, such as the GSA’s “Freeze the Footprint” mandate

- Technological: increased usage of mobile devices (e.g., tablets, smartphones) in lieu of real estate and human resources; also, usage of workspace monitoring systems to track desk utilization rates, reducing the number of idle workstations

- Generational: smaller footprints as a byproduct of tenants such as tech firms seeking to attract talented young workers with denser collaborative spaces and more flexible work arrangements

Today, corporate users are seeking to reduce the average space per employee to less than 200 square feet, and as low as 100 square feet in some cases. Although the trend of tenant downsizing will continue to result in a slower recovery in national office market conditions relative to previous cycles, further expansion in office-using employment bodes well for moderate increases in office absorption and rents in 2013. Office-using employment is poised to exceed the pre-recession peak by year-end, as a broader economic recovery bolsters demand from tenants outside of the robust ICEE (intellectual capital, energy and education) industries.