The following is an excerpt from a presentation I gave at the National Federal Development Association conference earlier this month in Washington, D.C. The presentation covered three themes: 1) The size of the federally leased property market is small; 2) It is getting smaller, and; 3) There are five factors that could return the market to future growth. This article profiles the second theme. To read about the first, click here. The final segment will be posted soon.

GSA Lease Inventory Trend

After a half-century of consistent growth, the federally leased property market is now getting smaller. From its peak at the end of 2012, the GSA-leased inventory has declined by 5.1 MSF. That’s only about a 2.5% reduction, but it is still the most significant downturn in the 50 years for which inventory data is available.

The graph’s modest downturn belies a steeper decline because, all things being equal, the GSA lease inventory would naturally grow. This is because in 2007 GSA dramatically restricted leasing delegations and since then its leasing responsibilities have expanded. Many of the leases previously executed directly by agencies are now transferring to GSA’s control upon their expiration. Further, some agencies have relinquished their statutory leasing authority (contracting authority provided by law).

One such recent example is the Transportation Security Agency (TSA). TSA was formed in 2001 by the Aviation and Transportation Security Act. That same legislation also provided TSA with the authority to acquire real estate, an authority TSA used to sign a 545,000 direct lease for its new headquarters in Arlington, Virginia. With that lease now approaching expiration, TSA has relinquished its leasing authority and engaged GSA to procure its replacing lease. When GSA finally completes this transaction, TSA will consolidate and downsize slightly into its new location, however, the net impact on the GSA lease inventory will be growth. Despite this, we will probably see the overall GSA lease inventory decline.

Anecdotally this seems especially probable when we look at the lease procurements that are just beginning because, in nearly all cases, some form of downsizing is planned. What’s causing this? The most direct answer is “Freeze The Footprint” and, more recently, “Reduce The Footprint” policy mandates from the Office of Management and Budget (OMB).

“Freeze The Footprint” is the name given to OMB’s May 11, 2012 memorandum, which ordered that agencies may not increase their inventory of civilian real estate above the level established in FY 2012. Earlier this year, OMB refined its guidance, requiring agencies to reduce their real property holdings by “prioritizing actions to consolidate, co-locate and dispose of properties.”

We can trace the roots of this austerity back even further to 2011 when the fiscal conservatives took control of the House of Representatives and wielded their prospectus approval authority to demand cost reduction of the nation’s largest leases. Now, whether due to congressional or executive action, the federal property market is beginning to react to these edicts.

Tightsizing

Tactically, how is the government accomplishing this downsizing? This photo of the renovated 7th floor of GSA’s headquarters tells it all…

Before it was renovated, this space was laid out in typical government fashion, with a center corridor flanked by private offices. The renovation caused two workplace transformations: First, you can see in the photo that there are no walled offices anywhere. Even GSA’s Administrator and her senior staff all work in open plan workstations. Second, if you look just beyond the people sitting in the foreground you see that those many of those workstations aren’t traditional cubicles. They are benching stations to accommodate mobile workers who may check in for a day–or part of a day–of in-office work. In fact, at GSA’s headquarters, if everyone showed up for work on the same day there would not be enough desks for them. Now, that is tightsizing! GSA achieved space utilization of just 82 USF per person with its redesign, which marks the extreme end of the efficiency scale. Yet, implementation of telework is one of the primary techniques the government is using to whittle at its space needs.

This brings us to the other way the market is getting smaller: lease terms are shorter. Implementing a tighter–and increasingly mobile–work environment is difficult to plan, it requires a challenging cultural shift in most federal workplaces and it is expensive to build from scratch. These planning and funding challenges have overwhelmed GSA and their tenant agencies causing them to kick the can with short-term lease extensions.

GSA Lease Expirations

Lease expirations have now piled up such that 25% of all GSA leases are expire this year and next, and half of all leases will expire in the next five years. So, logically, there are relatively few long-term leases that we can invest in.

Remaining Lease Term

This is especially evident when we go back and look at properties that are at least 85% leased by federal tenants. Of the 2,100 such buildings we track (comprising the entire GSA inventory and a portion of those other buildings leased under delegated or statutory authority) about 250 have 10 or more years of remaining lease term–this without regard for termination rights, which, generally speaking, exist in the vast majority of GSA leases.

Ignoring the smattering of really large leases in the first graph, we can zoom in a bit and also see that the bulk of federally leased buildings are 25,000 SF and smaller. If you are an investor that is interested in larger buildings with long-term leases, your investment possibilities become much more limited. There are only 157 properties that are at least 85% leased to the federal government, larger than 25,000 SF and have 10+ years of remaining lease term. Increase the property size to 50,000 SF and the number drops to 100. Move it to 75,000 SF and there are just 78 properties you can invest in. And so on.

This is a key observation because federal credit is worthless without substantial remaining lease term. Yet, this most crucial segment of the federally leased marketplace–long-term leased properties–is getting smaller.

Kicking the can among existing leases is a big part of the reason lease terms have generally grown shorter but another reason for the scarcity of long-term leased properties is that the build-to-suit pipeline has been reduced to a trickle.

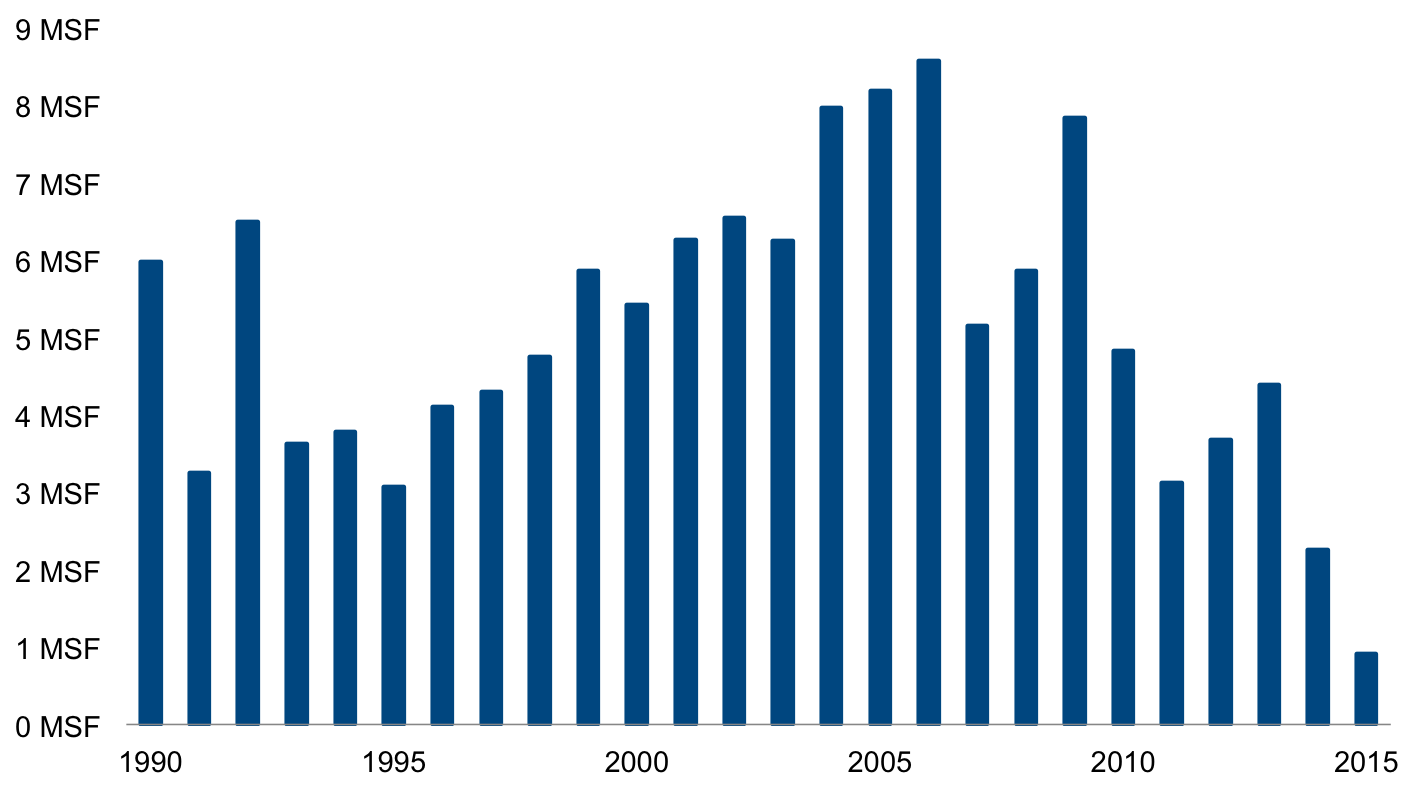

Dwindling Pipeline

The graph above shows the volume of federal leases in properties built or substantially renovated between 1990 and the present. The graph probably undercounts leasing volume in 1990s-era buildings where the tenants have since vacated and it probably also undercounts leasing in newer buildings that may occur in future years. Nonetheless, it is a pretty accurate representation of the trend.

Clearly, the volume of federal leases in new properties has fallen off dramatically. Among buildings built in the 2000s, GSA’s occupancy averages 6.8 MSF each year. Since 2010 that figure has dropped to 3.2 MSF. This is primarily due to a marked decline in build-to-suit activity. It is unfortunate because build-to-suits are the lifeblood of the federal investment sector. They yield generally longer lease terms than leases in existing buildings and the buildings themselves tend to be single-tenant and specialized, and they enjoy higher probability of renewal. Now they are disappearing and, without this pipeline of new long-term leased product to feed investors’ appetite for U.S.-backed credit, the market is feeling considerably smaller.

Federal Debt Held By the Public

{kind=link}

What is the root cause of this downsizing? For this austerity? It is in reaction to the growing U.S. national debt. The graph above, produced in August by the Congressional Budget Office (CBO), illustrates three things: 1) Debt has increased rapidly in recent years; 2) It is now the highest level since World War II, and; 3) Though it will decrease slightly in the near term, the long-term forecast is for continuous growth.

Today, the federal debt held by the public equals about 74% of GDP. In the short term that figure may decline slightly; however, over the next decade, CBO forecasts debt to rise to about 77% of GDP. From there the vector bends upward. In its long-term forecast published this Summer, CBO expects debt to eclipse the size of the economy in less than 25 years. And this forecast is the more optimistic of the two that CBO provides. The reasons for this dismal trend are unimpeachable structural factors including the aging workforce, increasing healthcare costs and rising net interest on the debt.

Maybe this doesn’t alarm you. Perhaps you are a faithful Keynesian who believes that more spending is the answer, even if it increases debt. There are many arguments for and against further spending and debt increases. Yet, none of it matters because, as long as there remains an influential contingent of fiscal hawks in Congress who view worsening debt as a threat to the nation, austerity measures will be imposed throughout government–including real estate leasing.

So, if debt is the real driver of the austerity that is negatively impacting the federal property market, how will property investors find relief? There are five ways the market can begin growing again. These are discussed in the next article.